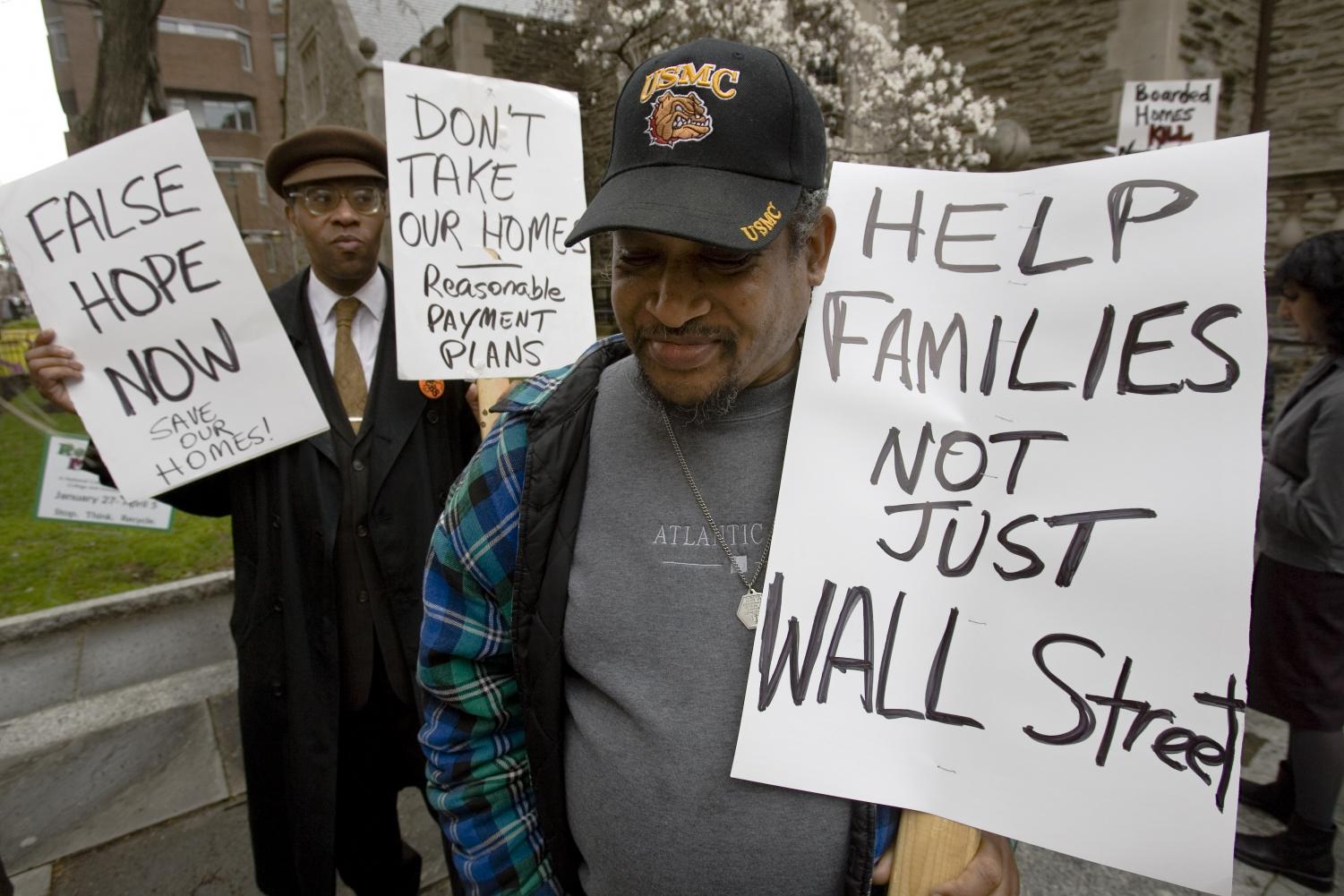

WASHINGTON — Under growing pressure from voters to do something about the nation's home foreclosure crisis, top Senate leaders agreed Tuesday to at least start with a plan that can win the support of both Democrats and Republicans.

The pact between Majority Leader Harry Reid, D-Nev., and Minority Leader Mitch McConnell, R-Ky., ended weeks of partisan bickering over what to do about the crisis in the housing market and the toxic effect it's having on the economy.

There is considerable common ground on several steps that can be taken to improve the situation, but battles over how to structure the debate had threatened to produce gridlock.

Reid agreed not to bring up a Democratic plan containing a controversial provision — strongly opposed by Republicans and President Bush — to give bankruptcy judges power to cut interest rates and principal on troubled mortgages. That plan stalled a month ago.

Instead, Senate Banking Committee Chairman Christopher Dodd, D-Conn., and the panel's top Republican, Richard Shelby of Alabama, were instructed to forge a compromise by Wednesday afternoon.

The legislation is likely to draw on elements of the Democratic plan such as letting states issue $10 billion in tax-exempt bonds to refinance subprime loans and permitting homebuilders and other money-losing businesses to reclaim previously paid taxes.

Democrats also want to provide $4 billion to states to buy up and refurbish foreclosed homes, a plan that the administration opposes as a bailout for lenders and speculators.

Senators in both parties gave the arrangement a 94-1 stamp of approval on a previously scheduled procedural vote. Sen. Jim Bunning, R-Ky., was the sole ''nay'' vote.

The upcoming bill also is sure to attract a GOP amendment by Sen. Johnny Isakson of Georgia to award $15,000 tax credits to people who buy and move into foreclosed homes. That would sharply boost demand, Isakson says. Lawmakers in both parties support the idea.

The measure is also likely to include a plan by Dodd to have the Federal Housing Administration guarantee perhaps $400 billion worth of refinanced loans if lenders reduce loan amounts to reflect reduced home values. The measure would force banks to make less money on the loans but would also reduce their credit exposure.

There is also bipartisan backing for $200 million in new money for debt counselors to help homeowners negotiate with lenders.

A floor battle still looms over whether to change bankruptcy laws to help borrowers trapped in subprime mortgages keep their homes. Sen. Richard Durbin, D-Ill., is the top backer of the idea, which has drawn withering opposition from banks, Republicans and a few Democrats.

Durbin said more than 2 million homeowners face foreclosure by the end of 2009, many of whom were duped into signing mortgages with unfair terms. The Center for Responsible Lending, which combats predatory lending practices, estimates about 600,000 people would keep their homes under Durbin's plan instead of ending up before bankruptcy judges who aren't permitted to adjust mortgage terms, regardless of how onerous they are.

The hotly contested provision rewriting the bankruptcy code, opponents say, would allow borrowers to effectively rewrite their mortgage contracts and would prompt lenders to tighten their standards and raise interest rates.

''It would mean higher risk, higher interest rates and higher monthly payments,'' said Sen. Lamar Alexander, R-Tenn.

''The mortgage bankers, God bless them, say this is the end of civilization as we know it … If these people go into court to be able to stay in there homes … interest rates will go up all over America,'' he said. ''Well, that isn't the case at all.''

Tuesday's developments don't guarantee a successful result, but both parties are under great pressure to produce a bill that can pass this year. There's enough common ground for a bill, even though difficult negotiations remain on several fronts.

As part of the breakthrough, Republicans agreed to not weigh the bill down with amendments unrelated to the housing crisis.

The progress comes on the heels of steps by the Federal Reserve to broker the eleventh-hour sale of a major investment firm, the failing Bear Stearns Cos., to a rival. It guaranteed some $30 billion in Bear Stearns assets, including questionable mortgage-backed investments. The central bank also allowed investment houses to get emergency loans previously reserved only for commercial banks.

The Bear Stearns deal greatly ratcheted up the pressure on lawmakers and the Bush administration, who faced the possibility of being portrayed as favoring huge investment titans over millions of people threatened by foreclosure.

''When it was clear that a major investment bank was in trouble, the Bush administration rushed to the scene like firefighters responding to a five-alarm blaze,'' said Sen. Robert Menendez, D-N.J. ''But a full year into the subprime mortgage crisis, they have done nothing but hit the snooze button on the alarm as millions of homeowners watch their dreams go up in smoke.''

Dodd said that about 8,000 homes are being foreclosed on every day.

''Foreclosures of this magnitude are on a par with the severity of foreclosures during the Great Depression,'' Dodd said. ''Each day without action means more are losing their homes.''